Last week, the Reserve Bank of India cut repo rates for the fifth consecutive time: a Diwali bonanza for home, auto and other loan borrowers. But this also means that FD interest rates will fall as well. Which translates into lower returns for depositors.

There was a time when any additional cash, like bonus or increment, was put in FDs. FDs were attractive because they used to pay in excess of 10 percent at one point of time.

Putting money in fixed deposits has been the traditional investment option, especially for those with low-risk appetite. Over time, the return on FDs has decreased due to a steady reduction in interest rates. So several investors are now considering debt-oriented funds.

Are debt mutual funds a substitute for FDs?

Debt mutual funds could give you better returns compared to bank FDs as India heads for a low interest rate regime. But tread with caution.

Let’s understand what debt mutual funds are with an example:

A friend of yours is starting a business. He requests you to lend him 10 lakhs for 2 years and will pay you an interest of 10% every year. Similarly, in debt mutual funds, money is lent to a corporate or the government for a fixed period of time and one gets remunerated for that period in the form of interest. Debt funds can invest in fixed income instruments like corporate and government bonds, corporate debt securities, and money market instruments that offer capital appreciation.

If things go well, your friend pays you the interest on time and after two years returns the 10 lakhs. But if the venture fails, it’s possible that your friend doesn’t pay you the interest and/or the principal. This is an example of Credit risk in debt funds. Which was in the news lately because of defaults by some companies like IL&FS, Zee Entertainment, DHFL and Reliance ADAG.

The second risk in debt funds is Interest rate risk. This is the danger that the value of a bond or other fixed-income investment will suffer as the result of a change in interest rates.

When interest rates go down, the price of these debt instruments tends to go up due to the inverse relationship between rates and bond prices, and will be a disadvantage when interest goes up.

How to mitigate these two risks?

Credit Risk: choose a fund that does not have a large exposure to a few corporate groups. Look for funds that are well diversified and do not lend more than 3-4% of the corpus to a single company or group and hold a majority of AAA rated securities.

Interest Rate Risk: invest in funds which lend for a short duration between 6-12 months.

A few other points to note

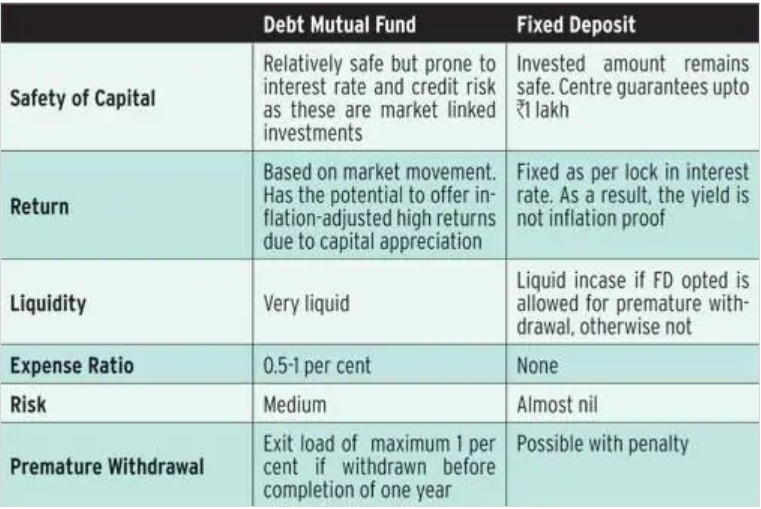

Liquidity: Say you make a one year FD but require the money in 6 months. The bank might charge you a penalty (0.5–1%) for premature withdrawal or pay you interest as per the interest rate applicable for 6 months.

With debt funds, some have an exit load (0.5%) if you withdraw before 3 months.

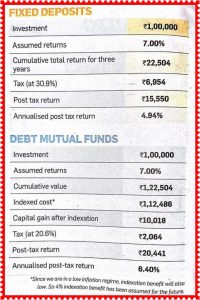

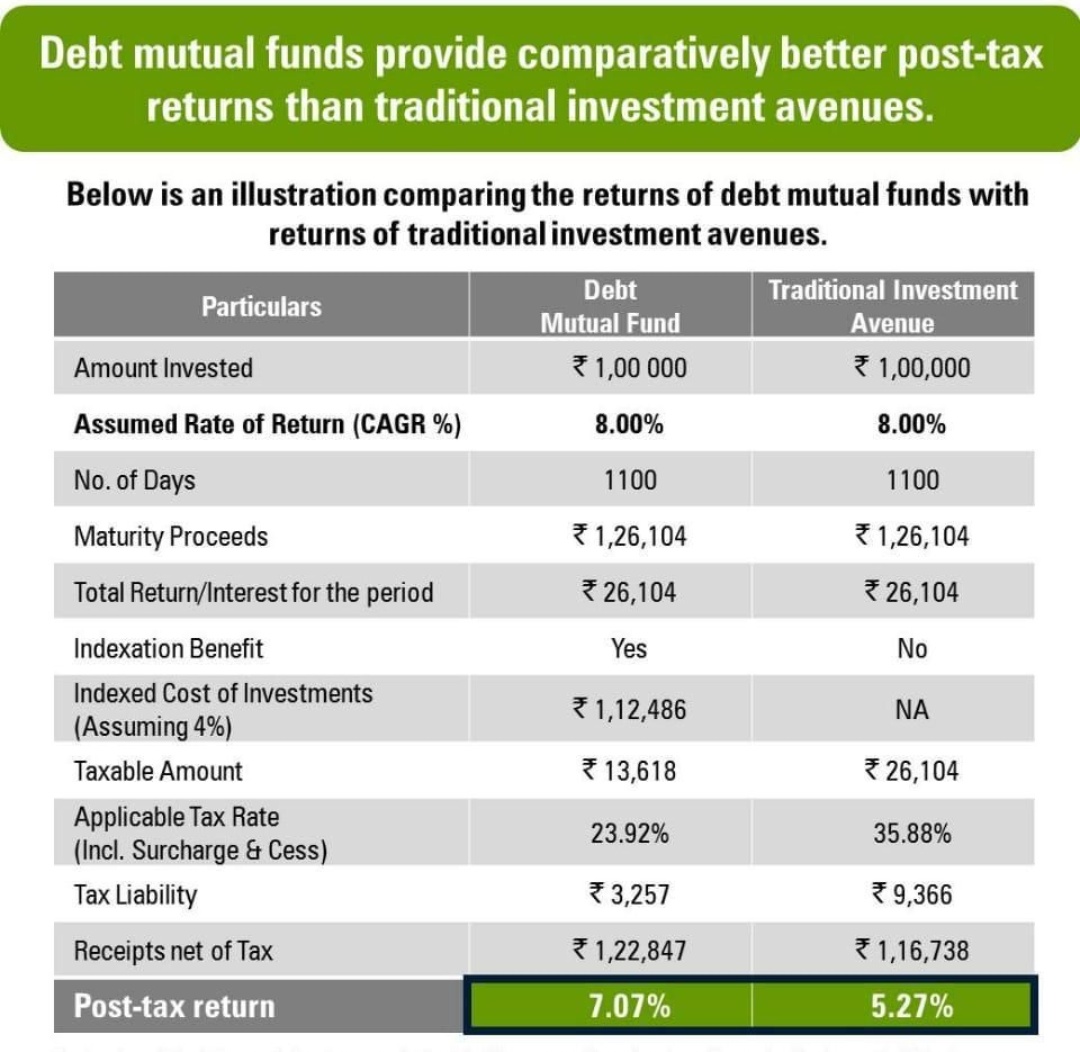

Taxation: Gains in FDs are taxed as per your tax slab.

Similarly the interest income in debt funds is taxable as per your tax slab if the holding period is less than 3 years (considered as short term). If you hold for 3 years or more, it’s taxed at 20% with indexation benefit. This is a game changer for investors in the 30% tax bracket (taxable income of over 10 lakh annually).

Debt funds also help in deferring the tax. With FDs, you have to pay tax on the interest every year. While with debt mutual funds, tax is payable only when you generate an income, that is, when the units are sold during redemption.

So the debate on FDs and debt funds is really more about making an informed decision considering your risk-taking ability, your immediate and long-term requirements.