New Year Resolutions! They come, they go, you feel bad when you forget about them a week after you set them. Did you make any New Year Resolutions this year? Were any of them related to your personal finance? Were they anything like these resolutions below?

Pay off my credit cards every month in full . . . with my other credit cards.

Save some money for a rainy day. That way I can shop online instead of having to go to an actual store.

Almost all of us have set resolutions, or have seen family, friends, or coworkers on the NYR path. So how do we make new year resolutions that we will stick to? Let’s get to the financial gameplan for this year.

Emergency Funds

If there’s anything that 2020 has taught us, it’s the importance of having some sort of emergency or savings fund. To give you a rough idea, you should have three or six months of living expenses saved up. But if you have zero savings at the moment, don’t try to collect six months of savings in one go. You have a better shot at accomplishing your resolutions and setting yourself up for future wins if they are achievable. So instead, make your goal that you’ll start an emergency fund in January and add to it each month in 2021.

Term Insurance

Your family needs your love and care. They also need financial security. As a provider, it is important to plan for the worst possible scenario as well, keeping in mind that that you may not be around to fulfill all their dreams, in the short-term as well as long-term. An effective way to do that is by acquiring a Term Insurance policy.

Risk is a part of life, especially in investments and finance. Your financial life can be flipped upside down by all kinds of surprises—an illness, job loss, disability, death or natural disasters. Insurance aids in protecting against unforeseen events that don’t happen often, but are expensive to take care of yourself when they do.

Health Insurance

A good mediclaim policy should usually cover expenses incurred towards all treatment related expenses like doctor’s consultation fees, expenses for medical tests, ambulance charges, surgery, hospitalisation expenses, and even pre and post-hospitalisation expenses to a certain extent.

When to buy Health Insurance?

You should buy health insurance before you run a risk of meeting with an accident or suffer a chronic disease that requires a major hospitalization. In other words, you should be covered under health insurance from the moment you are born till you die. This cover could be through your parent’s policy, your employer’s policy, your spouse’s policy, or your own policy. Choose a health insurance policy that matches your requirements in terms of coverage, deductibles, co-payments, etc.

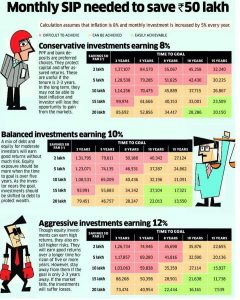

Automate Your Investments

The mistake many of us make is trying to wait for the right moment to start investing. Research has proven time and again that it’s impossible to time the market and so, with each year we delay; we stand to lose a lot in terms of wealth creation.

Instead, we can start investing in the financial product of our choice at regular intervals and let compounding do it’s magic. So for example, if you are considering equity mutual funds, then you can start investing via SIPs to build wealth steadily.

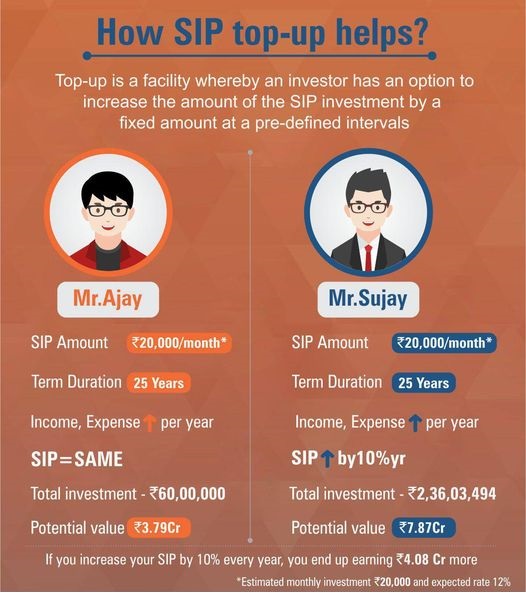

Top Up Your SIPs

What do you first think of when you get your annual salary increment? The first thought always tends to be about the additional expenses you can afford following the hike. But what about your savings? While you may have allocated a fixed amount for investments, such as mutual funds do you think about increasing the amount to match the hike in your income?

Ideally, you should top up your SIPs year-on-year, by say 10% or more. Take into account actual inflationary trends, lifestyle, and assess the future value of your financial goals. As you get annual increments, step-up your SIP installments.

Tax Harvesting

When it comes to tax planning, people usually think of investments under Section 80C like ELSS, LIC, PF etc.

Did you know you can realize up to ₹1 lakh of long term capital gains every year and not pay any tax on it? That’s a tax saving of up to ₹10,000 every year.

With the Indian stock market rallying after a sharp sell-off in March, your portfolio must surely have long term capital gains. It may be worth harvesting some gains if you want to lessen your tax burden. In this strategy you sell your shares or mutual funds such that your profit is 1 lakh or less. This way, your gain will be exempt from LTCG tax.

Click here to learn more “How to Save on Long Term Capital Gains Tax”.

Lastly, remember you don’t have to do everything at once. There’s a lot you can do to improve your financial health. Take one step at a time. Make some real progress on your journey this year.

The start of the new year gives us a chance to start over, to live this year better than the last. If you’re going to make just one resolution, make it this one: