Pawan is 35, he has three family members: his father, wife and daughter. Off late, his friends have been discussing health insurance, but Pawan is not particularly interested. He feels he has enough coverage by his employer sponsored health policy, which provides a cover of Rs 3 lakh.

Is a Rs 3 Lakhs coverage enough for a family of four, with a senior citizen or should Pawan revisit his health insurance needs? Pawan is certainly under-insured. His corporate health cover has stagnated and has not been revised. Sadly, he doesn’t realise this, and continues to feel that his insurance needs are met on the health front.

This is not a chance happening. It is possible your employer chooses to curb health benefits for you or your dependents. Or the entrepreneurial bug bites you and you leave your corporate job. Maybe you purchased a health insurance policy but it does not cover some illnesses for the first two years from the policy issue date.

It won’t happen with me

I’m healthy and strong so I don’t require health cover. Many of us overlook health insurance considering it an avoidable expenditure as they are in good shape. By God’s grace and your healthy choices, may you remain healthy. But this is one of the gravest errors that one can make financially. Regardless of how healthy you are, you have to have health insurance.

I have my company’s health insurance so I don’t need a personal one

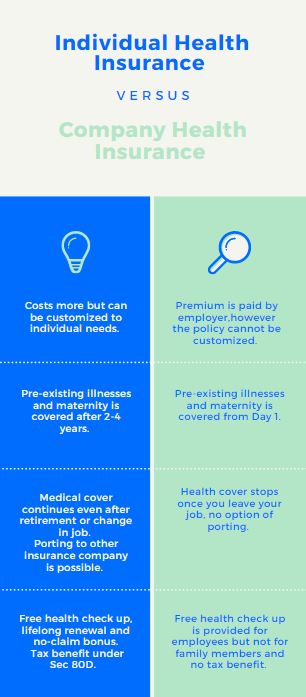

There is no doubt that the Employer’s Health Insurance has some wonderful benefits. Premiums on these policies are paid by the employer as against the policies bought personally. A major plus point is that even the pre-existing medical conditions are covered in these policies. An employee is not denied a Health Insurance policy because of higher age or any pre-existing conditions.

It provides many benefits but you can’t depend on it. We must ask ourselves “Is there enough cover for my family’s health?” or “Is the sum assured sufficient to meet medical emergencies?” before being content with only your company’s health insurance.

Change of Job

The key motive to have a private health insurance policy for you and your family is that, with a few exceptions, the majority of people don’t work for the same company their whole lives. You may change jobs only to learn that your new employer doesn’t provide health insurance. You may start your own business, which means no health benefits. Or you may, unfortunately, lose your job. You are not covered by any policy for the period between when you quit one job and start another. Though this one week or one month might appear to be a short span of time to cover, a medical emergency can happen at any time. Personal Health Insurance will have you covered in any case.

Limited or Insufficient Coverage

Group insurance policies come with a restricted coverage. The sum assured might be insufficient in the case of a severe illness. Your corporate health cover has a standard sum insured for all employees and their families. But your requirements might be different from others’.

An accident or major illness is adequate to inflict monetary mayhem. The number of dependents may also be restricted, which implies that not all your family members may be covered.

The right sum insured should ideally be based on your age, life stage, family structure, lifestyle, medical history and so on.

Many employer provided insurance plans have the room-rent capping and co-payment clauses, which can cause you to pay out of your pocket for medical care services. In the co-payment clause, a certain percentage of the bill has to be paid by the policyholder. The insurer is only responsible to pay a specified percentage. When buying a regular policy you can select one that has a bare minimum or no co-payment clause and offers higher coverage for hospital room tariffs.

I’ll buy the policy 2-3 months before I retire or quit my job

Temporary Exclusions: A Health Insurance policy usually opens up to full coverage in a staged manner. Here are some common waiting periods:

- Pre-existing illnesses at the time of buying the policy like diabetes or hypertension are covered after 2-4 years.

- A specific list of treatments that are not pre-existing like hernia, cataract or joint replacement are covered after 2-4 years.

- Illnesses apart from the ones above are covered 31 days after the policy is issued.

Hence it would make sense to buy a personal health insurance policy as soon as possible.

Getting an insurance policy becomes difficult as one ages

As you grow older, the risk of acquiring a lifestyle disease like diabetes or hypertension increases. Once you suffer from a chronic lifestyle disease, the insurer may hike premiums by 20-50% to cover the additional risk. To add to this, there’s a risk that your proposal might be declined altogether, and you may be refused a policy.

Imagine approaching your retirement date only to learn that you will not get affordable health insurance anymore. So, you have to choose whether to go without a health cover or pay an unreasonable premium for a mediocre cover!

Customization: Private Plans Come With More Perks

Not only do private health insurance policies provide you a range of different covers, but they also provide extra benefits. Private plans offer a free health check-up annually, lifelong renewal and a no-claim bonus of up to 50 percent for every claim-free year.

Portability of No Claim Bonus: If you opt for private health insurance, the bonus added can be ported if you decide to switch. This is not the case with a company insurance plan.

Tax Benefit

The premium paid toward your health insurance policy is tax deductible under Section 80D of the Income Tax Act. Though the main reason to buy insurance is protection, tax saving is always welcome. The limit for health insurance deduction under section 80 D is Rs. 25,000 and Rs 50,000 for senior citizens.