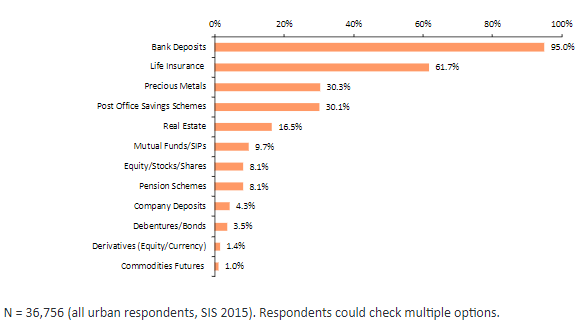

A couple of years ago, a survey was conducted to understand investment and saving avenues preferred by households in India. No major surprise that the majority of households preferred investing in Fixed Deposits, followed by Life Insurance products, Precious Metals (Gold) and Real Estate. Mutual funds came at sixth place, followed by stocks.

Even today, not much has changed. Whenever there is any major event in life like a wedding or birth of a child, the first thing we do is start an FD or buy an investment cum insurance product (endowment plan). Essentially a life insurance policy which, apart from covering the life of the insured, helps save regularly over a period of time so the policyholder is able to get a lump sum on maturity if he/she survives the policy term.

A friend who was recently blessed with a child, reached out to ask if he should invest in LIC Jeevan Tarun plan. An annual investment of 58,000/- for 20 years (so the total premium paid would be 11.53 lakhs) and the maturity amount will be about 33 lakhs with a sum assured of 12.5 lakhs.

It appeared to be a good investment option until we calculated the rate of return: a measly 7%.

Friend: Then what will be a good investment option?

I suggested investing in Mutual funds.

Friend: I’m not comfortable investing in MFs. It is risky as there are a lot of ups and downs.

I agree with you. There is volatility in the short term. But if you give MFs the same time as endowment plans, real estate or gold, there is zero scope of negative returns. And investing through SIP for longer tenures can significantly increase the amount of wealth creation.

This conversation made me realize that Safety is of primary importance after which come Returns.

With the help of data, let’s see whether this is true or is a salesmen’s selling pitch.

Safety

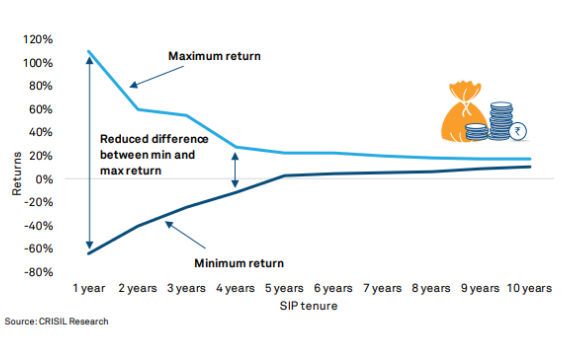

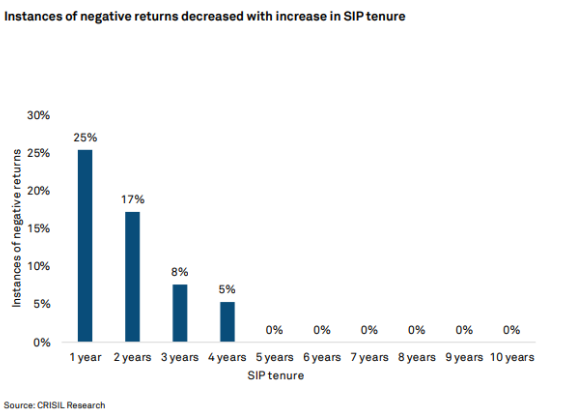

Let’s say you chose the worst time and mutual fund scheme for to invest in. Data shows that investing for the long term will iron out the effects of both flaws. The chance of negative returns in the first year stood at 25%. That falls to 17 percent if the holding period is two years and plummets to eight percent if the holding period is three years. The scope for negative returns reduces to five percent if the holding period rises to four years. And from the fifth year onward, there was zero percent chance of negative returns.

Returns

In the short term, the returns can vary quite a lot. But as the number of years pass by the difference between the minimum and maximum SIP returns also narrowed with the increase in the investment horizon.