Motherhood often implies that everyone and everything gets attended to except you, Mama. But when it’s time to plan your financial future, you must be a bit self-centered! Your children will appreciate and respect your financial independence later on in life.

Mothers usually prioritize the needs of their children, spouse, elders and their work above their own. There are only 24 hours every day and responsibilities like feeding the family and cleaning the house take precedence over less important things like understanding and planning for your financial future.

But doing this is almost as integral as providing meals and a tidy home and it takes up less time than either. The statistics suggest that on average, women outlive men by a decade, are increasingly earning additional incomes for their families, take more gaps in their careers due to motherhood and child raising. Hence there is a critical need to financially plan for the short, medium and long term.

Women are also more likely to take up part-time work or jobs without retirement benefits or become self-employed in order to keep their schedules flexible. Add to that the statistical likelihood of outliving your partner you’ve got the possibility of a long and possible less than optimal retirement. Below are some suggestions to face these obstacles and ensure you’re not slogging all your life.

As pressed for time as you are as a mom, it is suggested that you allocate a specific time and date regularly to do this.

The Statistics

- The average woman spends 15-20% of her career out of the workforce caring for her children and elderly parents. For each year out of the workforce, a woman has to work five years to recover the lost income, pension coverage, and career promotion.

- On average, women live longer than men, and at some point in their lives, 9 out of 10 women will be solely responsible for their finances.

Without their partners, some women suddenly find themselves on unstable financial ground. Too many women also neglect their finances, either preferring to let someone else handle them or simply postponing them indefinitely.

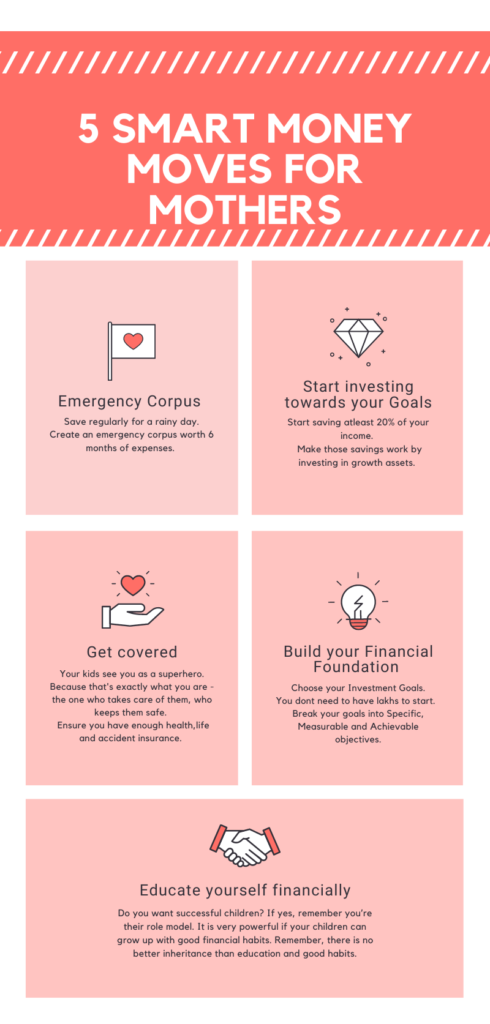

And the Smart Money Moves are:

Emergency Corpus

There might be some rainy days so umbrellas are important. Even a few thousand rupees saved monthly can build a considerable reserve – or an emergency fund. Why do you need an emergency fund? Should you or your spouse be unemployed, that cushion can help you through harsh times. Or if a family member suffers a major illness, the burden of paying for treatments will be reduced. Being a mother means being prepared for everything, including the worst.

Insurance

Ensure the primary earner has enough life and disability insurance to support the family incase something goes wrong. After all, the household is depending on that income.

Health insurance is not priority for women in India. A recent survey found only 39% of them had health cover. Of this figure, 22% had bought insurance for themselves, while the rest depended upon policies bought for them by male relatives or employers.

Women often get so engrossed in fulfilling family responsibilities and duties that they tend to forget their own good.

Establish Your Investment Objectives

Understand that you don’t need a stash of lakhs to begin investing. Your reason for investing will direct your investment decisions going forward. Your goals determine what you will invest in. It is advisable to break your goals down into specific, measurable and achievable objectives.

For example, “I want to have 2 Lakhs in my retirement account in three years.” Once you reach that goal, you can increase your target, maybe to saving 5 Lakhs, then 10 Lakhs, and then have 50 Lakhs before you turn 40.

Identify Your Risk Tolerance and Time Horizon

Your risk appetite and time horizon (how much time you have before you need the money you’re investing) are two key ingredients in determining the right combination of stocks, bonds and other investments, called your asset allocation. What is asset allocation and why does it matter?

Without planning for your investments, you will end of shaken by market movements. Risk tolerance is made up of two things: your ability to take risk and your willingness to take risk. You might have enough money to withstand the risk of a market decline, but if watching your valuations go up and down won’t let you sleep, your willingness to take risk may require a more conservative approach.

Consider consulting a professional. It doesn’t pay to save a little in fees only to lose a lot more with poor investment choices. Take the time to find a trustworthy financial advisor with who you’re comfortable, someone who can guide you during financial ups and downs with your best interest at heart.

Educate yourself financially

Do you want successful children? If yes, remember you’re their role model. It is very powerful if your children can grow up with good financial habits. They are likely to avoid future headaches and so will you. Remember, there is no better inheritance than education and good habits.

Tend to your credit rating

A healthy credit profile goes a long way in securing access to future loans and credit cards to make dreams a reality. With credit awareness on the rise, how can mothers boost their eligibility so that they are loan-ready to meet their financial goals?

Here’s how to create a positive credit profile:

- Applying for and accessing credit cards cautiously: Lenders may have various credit card offers (with cashback or credit points). But do you need to have multiple credit cards? Check out banks’ credit cards or loan products and start with one credit card only.

- Creating a credit footprint with a consumer durable loan: Taking a consumer durable loan (of a smaller amount) can be as easy as buying a smartphone or washing machine on an EMI-basis. Though this is a smaller EMI amount that can be repaid easily, it will create a credit footprint, and timely monthly payments will build a positive credit profile.

- Paying every single credit card bill and loan EMI on time: Paying all credit dues on time, every single time can go a long way in showcasing responsible behaviour and buliding an optimum credit profile.

Take an annual preventative health check up

As all doctors advise, go for an annual check of your full body if you are over 35 to ensure early detection of any impeding disease. For females, it is also important to cover checkups for the following: Cervical and Ovarian cancer. With early detection, a preventive course of action can be taken before it becomes chronic.

What are the biggest short-comings moms are guilty of regarding money?

Always putting their children ahead of themselves. Moms put everyone else – especially their children – first. It is a beauty of motherhood, but it can also really hurt us financially. If you have to choose between saving for your child’s college education and funding your own retirement, you should probably prioritize your retirement. Please remember there are education loans available but not retirement loans.

Excellent article as a gift to mothers , Happy Mother’s Day