It is commonly believed that having more money means an improvement in one’s personal finances. This could be so IF the additional income is managed well but that is not guaranteed. Very often, an increase in income is followed by an increase in expenditure. This is called Lifestyle Inflation. And it causes people to get stuck in the rat race of working just to pay the bills.

We live in one of the most affluent times in history. Cars, streaming television, smart phones and other electronic gadgets that we consider essential today would have been extreme luxuries (or even unimaginable) to our grandparents generation when they were growing up.

Why Lifestyle Inflation Happens

We have a strong tendency to spend more if we have more. One reason why is the “keeping-up-with-the-Joneses” mentality or for Millennials, FOMO, the Fear Of Missing Out. It’s quite common for people to feel like they have to keep up with their friends’ lifestyles whether we realize it or not. For example; if many colleagues start driving SUVs to the office, you might feel a very strong urge to buy one as well, even though your i10 is still working just fine.

We can also end up spending more than we need to (or should) on vacations, dining out, entertainment and wardrobes just to match our friends’ facebook updates.

Another cause of lifestyle inflation that can be tricky to gauge and overcome is the sense that you “deserve” some sort of perk or another: I deserve this expensive car. I deserve this expensive trip. I deserve this spa treatment.

But Wait, Isn’t It Good To Be Able To Enjoy My Money Now?

Absolutely! Increasing the quality of your life is a beautiful thing and something to be very proud of. But most people increase their spending as their income increases, without being thoughtful about the way they are spending. With this newfound awareness, What next? It can be a slippery slope, so if you find yourself itching to spend after your Diwali Bonus, try these tips to keep the money in your pocket.

Automatically Transfer Your increment Before You Can Touch It. Out of sight, out of mind: If you want to protect the extra cash you get from an increment or a new job, get it out of your bank account ASAP. Our future selves will be thanking us as the incremental SIPs will go a long way to match the higher expenses in the future.

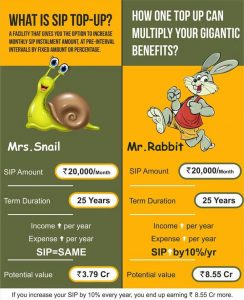

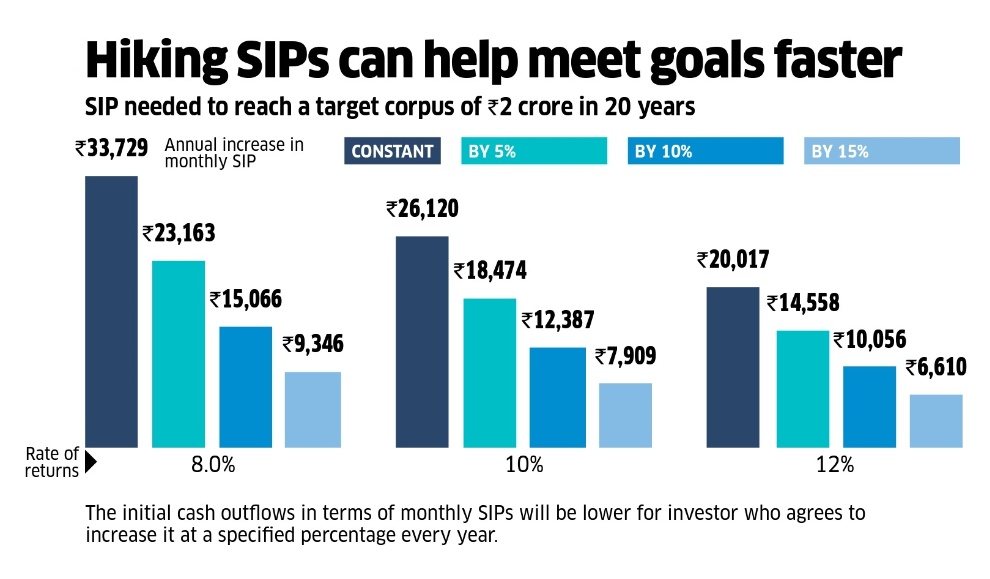

To make Rs 2 crore in 20 years with an assumed rate of return of 12%, if I am investing the same amount over twenty years, I have to invest Rs 20,000 monthly. If I increase my SIP by 5 % annually, then I can start investing with Rs 14,600. If I increase by 10% then I can start with Rs 10,000 and if the annual increase is 15% then I can start with as low as Rs 6,600.

Make Gradual Changes. There’s nothing wrong with improving your lifestyle as you earn more. But no millionaire became a millionaire by blowing extra money as soon as he got it.

Don’t Equate Success With Material Things. Feeling that you have the right to spend more in order to prove your success is tempting. Just remember the famous picture of Bill Gates and Mark Zuckerberg! US$138 billion in one frame and no Gucci belt, Armani suit, D&G shoes, Rolex watch, fashionable clothes or jewellery in sight! The goal is to be rich, not to look rich!

Create (and Stick With) a Splurge Budget. One really useful tactic I’ve found for keeping my splurges in check every month is a “hobby/splurge budget”. I cap how much I can spend on leisure, entertainment, shopping, etc.

While an increment is great, you can be just as financially stressed whether you’re earning 10 Lakhs or 25 Lakhs a year. The crux of the matter is that our expenses don’t actually increase as much as our income does. We raise it to that level with lifestyle inflation. If we were to invest the extra savings in Incremental SIPs, we could achieve our financial goals sooner, improve our lifestyle and increase our wealth in the long term.