Imagine for a minute that you’re thinking of buying a car. You’re very likely going to read dozens of online reviews, compare prices at various dealerships in town, and possibly time your purchase such that you can get the biggest discount.

A sad truth is, many people put more effort into checking out the reviews of the restaurant they are planning to go to on Saturday night than choosing the right product when it comes to reducing their tax burden.

Thankfully we all spend some effort to save our taxes but not as much effort in deciding the most apt product which suits our investment needs.

The window of opportunity to trim your 2020 tax bill is coming to a close very soon. You have 17 days left to organise your taxes and investments. People who wait till March to plan their taxes must be scrambling to make some investments to reduce their tax liability.

While you may manage to lessen your total tax outgo, it is important that your investments align well with your financial goals. If the impending tax deadline is making you feel a bit stressed out right now, relax! Take a deep breath and continue reading for your benefit.

ELSS versus PPF

During the tax-saving season, ELSS versus PPF is a very common topic of discussion. Conservative investors consider PPF better while proponents of equity investments cannot see anything beyond ELSS. Several clients and friends inexplicably ask about this comparison.

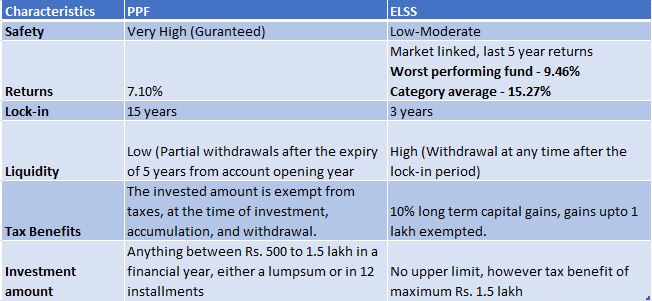

Apart from the fact that both PPF and ELSS offer tax benefits under Section 80C of the Income Tax Act, they have hardly anything in common.

ELSS is an equity product while PPF is a debt product. With PPF, returns are guaranteed while with ELSS, there is no such guarantee. ELSS investments have lock-in of 3 years while PPF matures in 15 years.

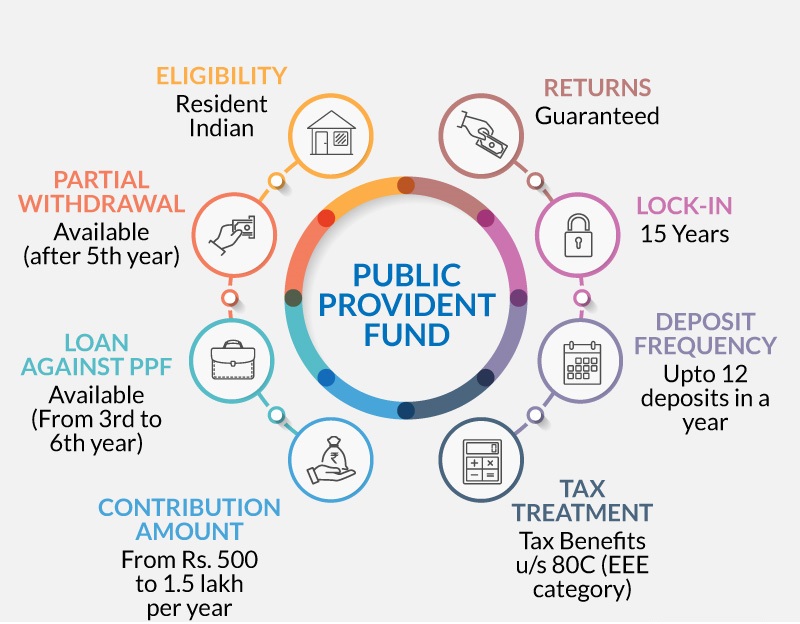

PPF

The Public Provident Fund scheme is one of the most popular long-term saving-cum-investment products, mainly due to its combination of safety, returns and tax savings. It is a long-term investment scheme with a lock-in period of 15 years. Individuals can start investing in PPF with a minimum amount of Rs. 500 p.a. The interest rate is set and paid by the government for every quarter. The current PPF interest rate is fixed at 7.1% which is compounded annually.

When considering investing in PPF or ELSS, it should be noted that the former is not available for Hindu Undivided Families (HUFs) and NRIs.

ELSS Funds

ELSS funds are equity funds that invest a major portion of their corpus into equity or equity-related instruments. ELSS funds are also called tax saving schemes since they offer tax exemption of up to Rs. 150,000 from your annual taxable income under Section 80C of the Income Tax Act.

The advantage ELSS has over other tax saving instruments is the shortest lock-in period of 3 years. This means you can sell your investment after only 3 years from the date of purchase! However to maximise returns from ELSS funds, it is recommended to keep your investments intact for the maximum duration possible.

Since ELSS mutual funds primarily invest in equities, they have the potential to generate reasonable market-linked returns. However, since the returns are subject to market volatility, one cannot be assured of guaranteed yields.

Which one is best for you?

This actually depends on what kind of investment you are looking for.

Taxation

The public provident fund enjoys the EEE tax benefit where the invested amount has a tax deduction under Section 80C up to Rs 1.5 Lakhs a year. The interest earned and the amount withdrawn at maturity is also tax free.

You incur a long term capital gains tax of 10% on ELSS capital gains in excess of Rs 1 Lakh a year. It’s widely believed that the EEE benefit makes PPF more tax-efficient than the ELSS.

ELSS schemes can yield double-digit returns, which even after the LTCG tax is higher than the returns from the PPF. This makes it more tax-efficient than most tax-saving instruments. Investors can maximize their tax benefits by harvesting tax exempt capital gains (of up to Rs 1 lakh) every year after the lock-in period.

Lock In Period

A PPF account has a maturity period (lock-in) of 15 years. ELSS funds on the other hand have a lock in period of only 3 years. But hold on.

Assuming you make annual investments in PPF, only your first installment in locked-in for 15 years. The 2nd year installment is locked-in for 14 years. The 3rd year installment is locked-in for 13 years…and so on. Also, the PPF accounts that have completed 15-year lock-in and have been extended have a fresh lock-in of 5-years.

Liquidity

Liquidity is an important consideration for many investors and rightly so. Tax savings should not imply that you keep your money locked in for long periods of time. The minimum tenure of PPF is 15 years, extendable in blocks of 5 years. Withdrawals not exceeding 50% of 4th year balance are permitted after a lock-in period of 7 years. PPF also offers loan facilities in specific circumstances.

ELSS mutual funds, on the other hand, are the most liquid investments u/s 80C. You can redeem your ELSS units partially or fully after the lock in period of three years is complete.

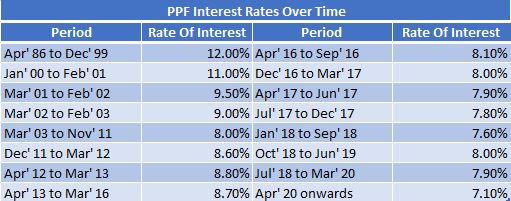

While PPF are interest-bearing instruments, the rate of interest itself changes – each quarter. So while the current rate of PPF at 7.1% seems attractive, know that it can drop. Though PPF doesn’t come with market risk, it has interest rate risk attached to it.

PPF, for instance, used to be at 8.7-8.8% between 2012-2015. PPF rates have gradually come down over the years and the 10%-plus rates of the 90s are a thing of the past.

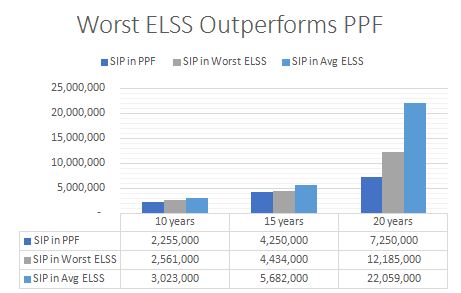

2, Total Investment after 15 years: Rs 22,50,000

3, Total Investment after 20 years: Rs 30,00,000

But remember, PPF is a debt product and ELSS is an equity product. All goal-based investment portfolios are best constructed by diversifying across assets.

You should not be 100% in equities or 100% in debt. Neither way is sensible.

For most people, the best approach is to invest in line with your goal requirements.

Taxes can take away a substantial amount of your income. Therefore, it is advisable to look for tax-saving investment options suiting your financial goals, risk appetite and investment horizon.