How did you choose which day of the month your SIP should be effected? A lucky day, Salary Day or the closest day from the day you started the SIP?

Instead of investing on a fixed day every month, what if we wait for a day when the markets are down (say by 2%) to invest, thus giving you a ‘lower’ price of entry as compared to a random price that the fixed day SIP might give. Seems like a better idea, doesn’t it? All of us can make assumptions and hypothesize but what does the data say?

Why a 2% dip you might ask? Why not 1 or 3%?

Because 1 percent would be too common (so our results would be very similar to a regular SIP) and 3 percent would be too seldom (we wouldn’t invest for very long periods of time).

In order to analyze this strategy we also need to decide what happens if there is no day with a 2% drop in a particular month? In that case, do we invest on the last day of the month regardless of the price or skip that month entirely and wait till the day when the market falls 2% or more, however long that may take?

Let’s compare three investment strategies:

1. Plain SIP

You invest 10,000/- monthly on the last day of the month.

2. Buy The Dip, Else End Of The Month

Every month, invest on a day when the market is down by 2% or more. If there is no such day, invest on the last day of the month.

Let’s compare our ‘triggered’ SIP to the Plain SIP

The difference between the two will occur only in months where there is a 2% down day. So the question then becomes that in such months, on average, is the price at the end of month higher or lower than the price when there was a 2% fall? If it is higher, then our triggered SIP is better as it gives a lower price of entry on average for such months. If the price is lower at the end of the month, then the Plain SIP is better.

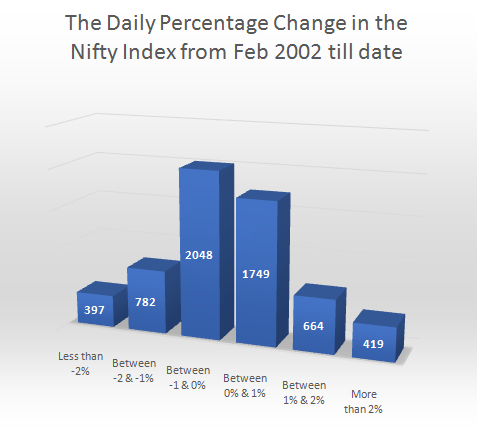

The historical data from January 1996 till date indicates that of the 292 months from then till now 161 months had at least one day when the stock markets were down 2% or more. That’s about 55% of all months – enough to make a difference if there is one. The remaining 45% of the months did not have a single such drop day.

3. Only Buy The Dip

We invest only when the market is 2% down. Skip months and wait for a 2% down day regardless of how long that may take. This is the more purist approach. Instead of investing every month, we only invest in months when there is a 2% fall (55% of the total) and we skip the remaining months (45% of the total).

If you attempt to build up cash and buy at the next bottom, you will likely be worse off than if you had bought every month. Why? Because while you wait for the next dip, the market is likely to keep rising and leave you behind.

Sometimes investors want to save up cash to “buy the dip” when they would be far better off if they just kept buying. One doesn’t realize that the beloved dip may never come. And while he or she waits, they can miss out on months (or more) of continued compound growth.

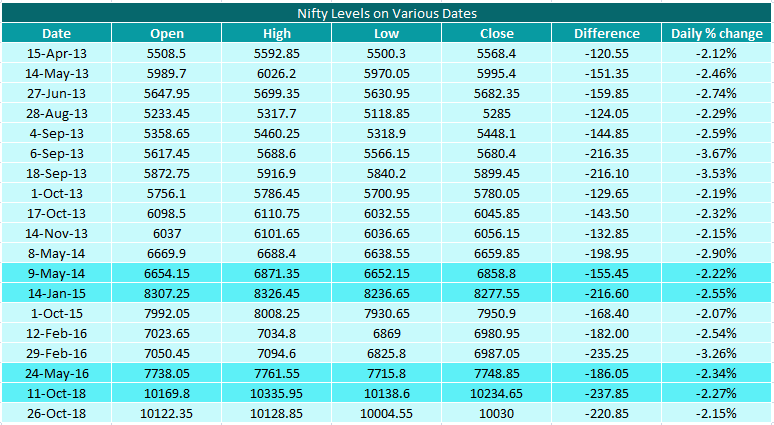

As you can see in the table below: with the Only Buy the Dip strategy, one misses out on months, sometimes a year or two of growth with the market rising by a few thousand points.

There were only 2 days in the 2014 when the market fell by 2 or more percent, namely the 8th and 9th of May 2014. An investor following the Only Buy the Dip strategy would buy at a market level 6858.8 points on 8th May 2014. As the next dip would be on 14th January 2015, he would make his next purchase at a market level of 8277.55, after a huge 21% increase!

Similarly, there wasn’t even a single 2% drop in 2017. From a market level of 7748.85 on 24th May 2016, the next purchase would occur at a level on 10234.65 on 11th October 2018. That is a staggering 32% leap.

The Result

Would the time and effort taken to execute the triggered SIPs in either Options 2 or 3 be worthwhile? It appears not.

The million dollar question is: When the market corrects sharply, will you have the courage to invest at that time?

On 23rd March 2020 occurred the biggest single day fall in the history of the Sensex: the markets fell by 13% due to the Coronavirus pandemic. Did you invest? How was your stomach when you learnt of this drop?

Is there a best of both worlds? A combination of the strategies? One option is to invest regularly and invest any surplus cash when there is a drop.

To conclude, as legendary investor and former Fidelity Magellan fund manager, Peter Lynch said as far back as the mid-1990s: