Have you ever dreamed of leaving your job? Imagine every day was a weekend: You could enjoy a lazy brunch with the family, go to Lonavla for a drive, play cricket with friends in the evening…

Most people are not happy working in a job and would like to retire early. They dream of an early retirement at 50, 40 or even younger. But they are unsure about how to plan for an early retirement.

Retirement planning is tricky enough when you plan to work until your retirement age. Even more so if you want to stop working years, or even decades, earlier.

Whether you want to have an Early Retirement or not, Financial Freedom is useful for anyone who wants to ditch the 9 to 5 routine.

One can find online: various retirement calculators, opposing viewpoints from countless financial advisers, volatile inflation and a broad spectrum of earning and expenditure patterns among readers.

We have reviewed retirement in “Wake Up! It’s time to plan your retirement with SWP.”

Because of this flood of information, people tend to become overwhelmed and say things like,

“All this is well and good for you but how can I know when I’ll have enough to retire with a completely different lifestyle?”

Now here’s the surprise: Your time to reach your retirement depends on only one factor!

Your Savings Rate as a Percentage of your Take Home Pay.

To understand better, your savings rate is determined entirely by these two things:

1, How much you take home each year.

2, How much you can live on.

While these numbers are quite simple to compute, the magic lies in the relationship between the two.

If you are spending all (100%) or more of your income, you will never be ready to retire, unless someone else is doing the saving for you (spouse, wealthy parents, PPF, etc.) So you will work forever.

If you are spending none (0%) of your income (you somehow manage to live for free), and can maintain this after retirement, you can retire right now.

Between the two extremes, there are some very interesting considerations. When you start saving and investing your money, it starts earning money of its own. Then the earnings on those earnings start earning more money. So this income grows exponentially.

As soon as this income is enough to pay for your living expenses, while leaving enough of the gains invested each year to keep up with inflation; you are ready to retire.

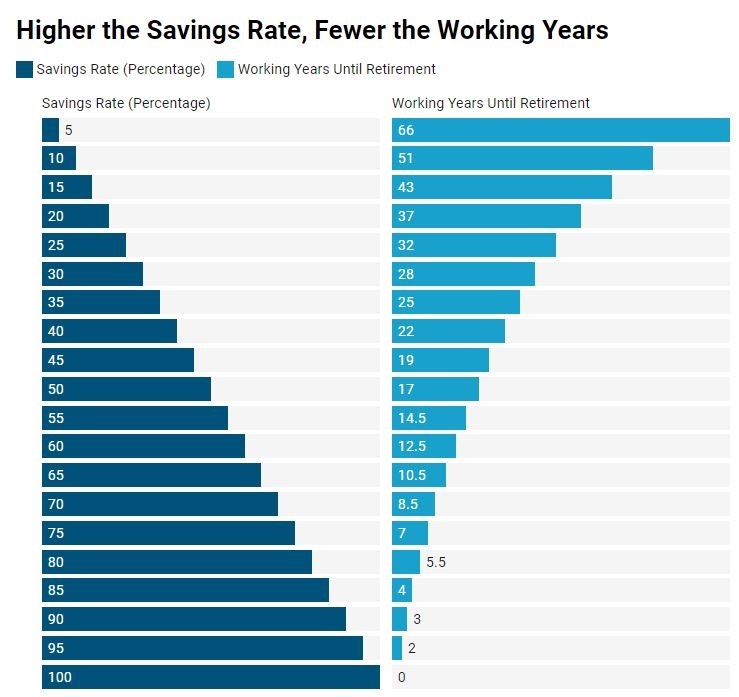

If you save a reasonable percentage of your take-home pay, say 50%, and live off the other half, you’ll be financially independent in 16 years.

With a few conservative assumptions, The table below will give you an approximate idea of how many years it will take you to become financially independent.

Assumptions:

- You can earn 5% investment returns after inflation during your saving years.

- You will live off of a 4% withdrawal annually after retirement; with some flexibility in your spending during recessions.

- As you want your nest egg to last forever, you’ll only be touching the gains, not the principal.

The table below shows how long you will have to work for a range of possible savings rates, starting from a net worth of zero:

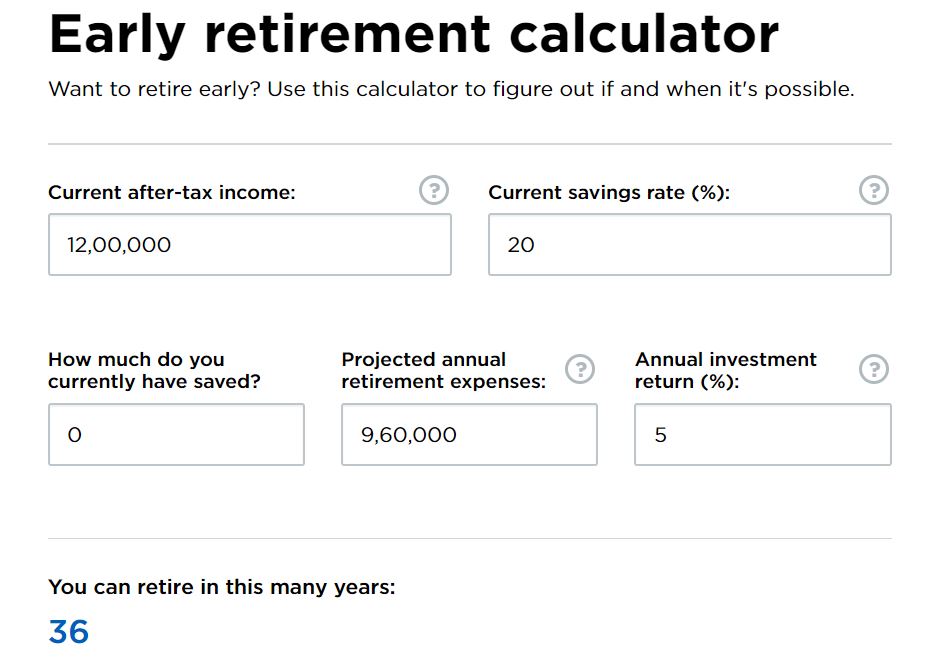

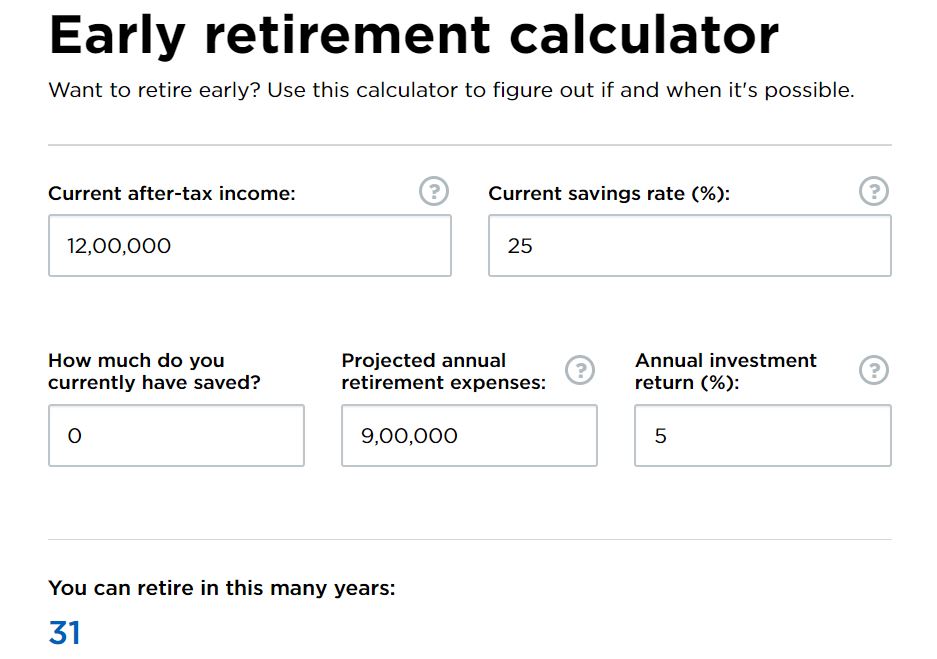

It’s fascinating that a middle-class family with a 12 Lakh take-home which saves 20% of their income is sadly on track for having to work for 36 years. But cutting a few dine outs and movies at the theater can boost their savings to 25%, allowing them to retire 5 years earlier!

It’s very important to enjoy life and make memories along the way but are those outings worth having two income earners each work an extra 5 years for?

The most important thing to note is that cutting your spending rate is very powerful! The reason being every permanent drop in your spending has a double effect:

1, It increases the amount of money you have left over to save each month.

2, It permanently decreases the amount you’ll need every month for the rest of your life.

Some people are able to leave full-time work because their expenses are low, not because they are rich.

The amount you need to save for a secure early retirement is dependent on your level of spending. If you have low annual expenditures, a smaller retirement nest egg will cover your costs. Earning a high income can help you achieve an early retirement, but only if you keep costs low and save a large proportion of your income.

If want to retire within 10 years, the formula is on your screen – simply live on 35% of your take-home pay. Sometimes, people are paralyzed by how it can’t be done, rather than figuring out how to do it.

Many retirees regret having devoted so much time and energy to their work and not enough to making enriching memories with their loved ones. By retiring early, you will have more time for your spouse and children. You might try to launch a business idea or tackle a project you’ve long dreamed of such as building your own farmhouse.