Ankit and Divya, both working professionals, spent considerable time over the last six months visiting several residential projects and finally zeroed down on their dream house. They took a home loan to fund their purchase. Fast forward a couple of years, now the family’s primary goal in life is to pay off this home loan as quickly as possible.

This is a story that plays out in countless households. There is pressure from the family to stop paying rent and buy your own house. Once the house is purchased, then there is an obsession to pay off the home loan.

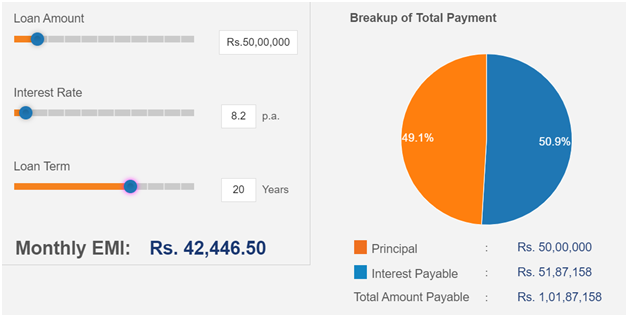

A typical 50 lakh home loan at 8.2% with a 20 year loan term will have a monthly EMI of Rs. 42,500/- and the total amount payable over these 20 years is 1.02 crore, that is, an interest of nearly 52 lakhs.

The interest paid over the 20 years will be nearly 52 lakh which is more than the principal borrowed from the bank. And this is the primary reason we like to prepay our home loans.

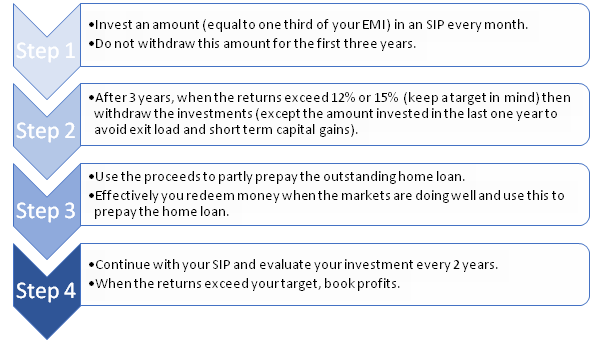

So how can we prepay the home loan?

Ideally the combined EMIs of all your loans should not be more than 40-45% of your total income. Hence after paying your EMIs and taking care of your expenses you should be able to save 10-15% of your income. Since we are left with 10-15% every month, we have the option of using this money to prepay the home loan. We should, however, take a few things into consideration before we rush to prepay the home loan.

We get tax deductions on the principal portion of the EMIs paid for the year upto Rs. 1.5 lakh. The interest portion of the EMIs paid for the year can be claimed as deduction from your total income, up to a maximum of Rs. 2 lakh.

Even if we consider only the savings on the interest portion, the effective tax rate will be below 7%. So if we can generate more than 7% on this amount, it is smarter for us to invest that money in an instrument earning more than 7% instead of prepaying the home loan.

Ideally one should continue with their home loan as the interest charged is less than 8.5% and equity mutual funds deliver more than the housing loan interest that one pays. However when the markets go down, investors feel that instead of investing in mutual funds they could have paid off their home loan.

Many of us know the story of Abhimanyu from Mahabharata.

Whilst still a baby in his mother’s womb, Abhimanyu learns the knowledge of entering the deadly and virtually impenetrable Chakravyuha from Arjuna. The epic explains that he overheard Arjuna explaining this to his mother from the womb. Arjuna spoke about entering Chakravyuha after which Subhadra dozed off. Arjuna stopped explaining how to escape from the Chakravyuha as he saw Subhadra sleeping. As an result, the baby in the womb, Abhimanyu, didn’t learn how to come out of it.